{kind=link}

I have a simple mental model for financial services and blockchains.

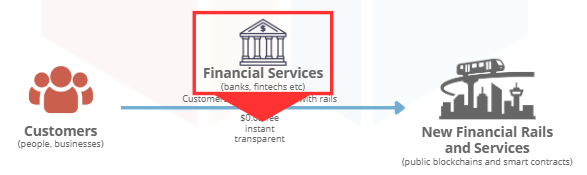

Before blockchains, customers (people, businesses) would instruct their bank, which would interact with financial rails to execute the instruction. Customers did not have access to financial rails directly. Banks would intermediate between customers and rails.

Banks would charge the customer, pay their costs, and make money. Customers had no choice but to interact with their banks, which all charged similar fees for basic services such as payments and foreign exchange. The banks were happy with their profit margins.

Then remittance companies and fintechs came along, and competed with banks on cost and speed. They typically leave money in bank accounts destination countries, so that it’s already close to where their customers want it, effectively pre-funding their customers needs.

But the fintechs still needed banks as their “rails”.

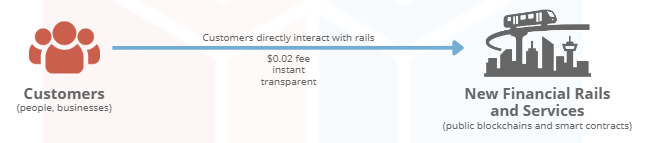

Then public blockchains came along, and for the first time in history, people and businesses could interact directly with the financial rails. They could store, send, and receive money/value with anyone anywhere in the world – so long as the other person was also crypto-competent.

There were cold start problems (both parties need to be crypto competent, and it works better when both parties are willing to hold value in onchain assets rather than needing to on/off-ramp for each transaction). The experience was raw, and in many ways, still is.

But it is getting better.

Public blockchains are scaling (faster, cheaper, more throughput), the user experience is getting better, cybersecurity is improving, key management is improving, and users are becoming more comfortable with new tools and methods.

So anecdotally, and proven by early data, people and businesses are turning to blockchains for basic financial services. Starting with domestic and cross border payments, and increasingly investments, treasury management, and borrowing and lending (collateralized, for now).

This echoes the move from banks to fintechs. But in that case the rails didn’t change, the banks still had control over the rails. (And as time passed, the fintechs became the banks: you either die a hero or live long enough to become the villain!). Today, blockchains are the new rails.

So where are we now?

As existing financial intermediaries sense competition (after all, a blockchain based payment can be up to 10,000 times better/faster/cheaper than using traditional rails, depending on the use case), they are reacting. Existing service providers and intermediaries are trying to innovate – as they should! They should always be trying to improve their offerings, reduce their costs, become more efficient.

But

“It is difficult to get a man to understand something, when his salary depends on his not understanding it.” – Upton Sinclair

Here’s how many (not all!) incumbents are looking at the problem, with respect to blockchain initiatives:

They are thinking “Hmm, how can we use blockchains to reduce our own costs, solve our own problems, make things more efficient for us? How do we inject ourselves between our customers and the blockchains?”. Intermediation is so ingrained that it is hard for them to think any other way.

This is why I call this “reactive re-intermediation”.

They’re missing the point! The point, of course, is that these new rails are designed for end users. So what is important is what the end users want; not what the intermediaries want.

Here’s my challenge to incumbents: Even if you can’t yet feel it, the new rails keep improving and people and businesses are moving in one direction. Your customers are becoming increasingly comfortable to interact directly with the rails. (trigger warning) You can’t keep charging $25 for a $0.02 transaction forever. Yes, you can re-intermediate. But you have to give value to get value. So what are you doing to keep your customers happy to keep paying you, instead leaving you to go directly to the rails? What are you giving them that they can’t get or won’t get from DeFi? Is this improving the state of financial services overall? Is this sustainable?

I’m hopeful that as this all shakes out, new business models emerge and customers win.